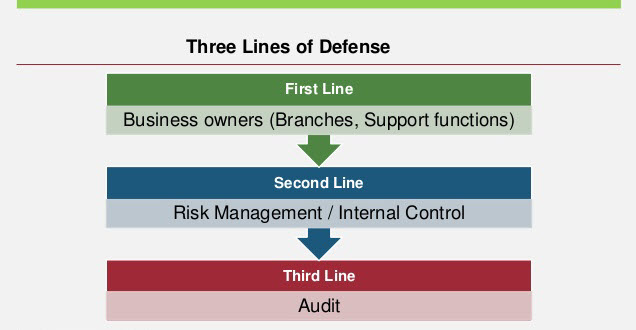

Here’s a good description of the ‘lines of defense’ approach that many financial institutions are taking to quality control, operational risk management and compliance risk management. Without a framework like this, it becomes much more difficult to meet today’s enhanced regulatory scrutiny, increasingly complex regulatory requirements and rapid pace of regulatory change.